This week, the total inventory of construction steel continued to increase, but the overall growth rate narrowed. Rebar inventory increased by 15.93% WoW, while wire rod inventory rose by 13.01% WoW. Supply side, blast furnace steel mills maintained normal production, and EAF steel mills gradually resumed operations. However, due to the incomplete resumption of steel scrap processing bases, the operating rate and capacity utilisation rate of electric furnaces remained relatively low. Demand side, although enterprises gradually resumed work and production after the Lantern Festival, demand recovery still required time, and the market remained cautious.

This week, the total rebar inventory was 7.6652 million mt, up 1.0535 million mt WoW, an increase of 15.93% (previous value +47.62%). YoY, it decreased by 3.3143 million mt, a decline of 30.19% (previous value -32.64%).

Table-1: Overview of Rebar Inventory

Source: SMM

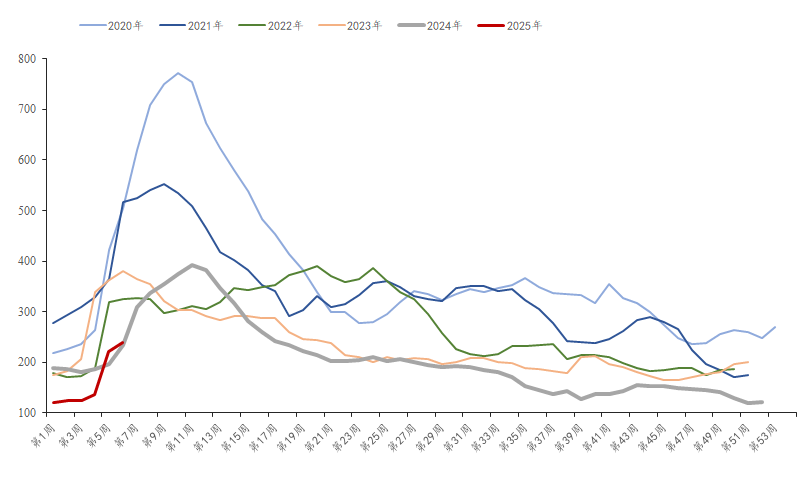

This week, in-plant rebar inventory was 2.3875 million mt, up 175,000 mt WoW, an increase of 7.91% (previous value +62.30%). YoY, it decreased by 977,000 mt, a decline of 29.04% (previous value -28.36%). Currently, blast furnace steel mills are operating normally, and EAF steel mills are gradually resuming production after the holiday, leading to an accumulation in factory warehouses.

Chart-1: Rebar In-Plant Inventory Trends, 2019-2024

Source: SMM

This week, rebar social inventory was 5.2777 million mt, up 878,500 mt WoW, an increase of 19.97% (previous value +41.19%). YoY, it decreased by 2.3373 million mt, a decline of 30.69% (previous value -34.61%). Currently, although downstream sectors are gradually resuming work, market demand has not fully recovered. Social inventory continued to accumulate, but the growth rate narrowed.

Chart-2: Rebar Social Inventory Trends, 2019-2024

Source: SMM

Overall, supply side, EAF steel mills have gradually resumed operations, with most electric furnace plants restarting after the Lantern Festival, and supply is expected to increase further. Demand side, downstream markets have resumed work and production, but the end-use market's resumption rate and labor attendance rate remain lower than last year, and market operations are still cautious. In the short term, the market is expected to remain supply-strong and demand-weak, and construction steel inventory is likely to continue accumulating next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)